Gerber Life Final Expense Insurance Review

Buy Life insurance from Gerber Life without answering any health questions

Gerber Life Insurance was introduced in 1967 which as a subsidiary of the Gerber baby food family business. It all started in 1927 when Dorothy Gerber was preparing baby food for her infant child and an idea was born. Not long after, Gerber baby food went into production one year later in the family owned canning factory. In order for them to sell the new idea, they issue coupons with the all familiar picture of the Gerber baby which is the familiar face we all know and recognize.

Within 6 months they were a national brand and sold over a half million jars in the first year. Not much later they branched out and were selling other baby related products like clothing and skin care. It wasn’t until 1967 that the Gerber face was associated with life insurance for children.

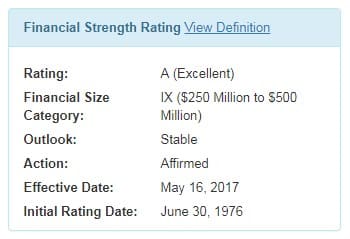

Today the Gerber Life insurance Company, now a completely separate entity from the Gerber Baby Products company insures more than $45 billion dollars of coverage and as of May, 2015, A.M. Best has rated Gerber Life Insurance an A (Excellent).

Gerber life has a several life insurance plans for children starting at birth and more recently Senior Guaranteed Acceptance Whole Life insurance. The products are competitively priced and a good value for the money. If you are looking for yourself late in life, consider purchasing it for your children or grandchildren too. Gerber Life is is one of the best Final Expense Burial policies on the market today.

Guaranteed Acceptance with Gerber Life Final Expense Insurance

- Whole Life insurance for ages 50 – 80

- Death Benefit from $5,000 – $25,000 to age 121

- Acceptance is guaranteed

- Builds cash value

- Rates will never increase

- Available in all states except Montana

For the kids…The Grow-Up plan (Available for Parents and Grandparents to purchase)

- Whole Life insurance for ages 14 days to 14 years

- Death Benefit from $5,000 – $50,000 to age 121

- Acceptance is not guaranteed* (see below)

- Coverage doubles at no extra charge at age 18 with no premium increase

- Builds cash value

- Guaranteed optional increases with no health underwriting at ages 21, 25, 30, 35 and 40 up to a total of $450,000

*The Whole Life Grow-Up plan is not a guaranteed acceptance life insurance policy. Limited health underwriting applies.

The Gerber guaranteed acceptance life insurance is one of the best priced burial or “Final Expense” plans with no health questions, but you may be able to get better benefits. There are two general areas to consider when comparing final expense burial insurance.

First and foremost is the cost. What ever you decide to go with, it should be an amount that you know you can afford. You need to make it a priority like paying an electric bill. There is no sense in buying a life insurance policy that you “should be able to handle”. Be absolutely positive that you will pay the premiums even when the car needs fixed or Christmas comes around. If you don’t, you’re just wasting money.

Gerber doesn’t ask any health questions, but you do pay the price for that. It’s very likely that you will get more for your money or lower premiums if you go with a company that you have to pass a few health questions. If your have some health issues as most of us do, our independent agents can help figure out which companies would approve you and compare the rates.

Second is what gets paid when you die. The death benefit from a Gerber Life Guaranteed Life policy is “Graded”. This means that if you die in the first 2 years of the policy effective date (the date your coverage begins), your beneficiary will get back the money that your paid in premiums plus 10% interest no matter how much death benefit you purchased. After the policy has been in force for 24 months, it will pay the entire death benefit.

There are a lot of us that just won’t be able to pass the health questions concerning health conditions like COPD, heart disease, cancer and Kidney disease for any company. If that’s the case, Gerber is one of the best deals available. The idea is to make sure you can’t get a policy that pays out more to your beneficiary than a return of premium plus interest. Even if you have been turned down before, Gerber will still grant you the coverage so it’s a true guarantee. If you pay for it, you can have it!

Gerber Life ratings in the life insurance industry

Gerber earns an A rating, only 2 levels down from the best from A.M. Best rating. A.M. Best is the industry’s authority on the financial stability of insurance companies. There are 13 possible ratings from the best possible score of A++ down to D indicating a poor ability to meet future insurance obligations.

Payment Options

Gerber Life is one of the few companies that will accept a payment by a credit or debit card as an alternative to debiting your savings account or checking account. If you just won’t let any company take a payment automatically, then you can even pay by sending in a check or money order either monthly, quarterly, semiannually or once a year. Keep in mind you’ll pay a little more to get that paper bill, but at least it’s an option.

Should you purchase a Gerber Life Final Expense Insurance policy or just put the money in a savings?

It can be difficult to understand the concept behind burial policies that have a graded or modified benefit for the first two years. The rationale behind just putting the money aside doesn’t really make any sense because know one really know when they will die. Actually, if someone has a terminal illness, then it makes perfect sense to purchase any life insurance policy other than an accidental policy. The less time a person lives, the higher the payout because how else can you turn $2,000 worth of paid premiums into $20,000 in just a few years?

Think of it this way…you might spend the same amount of money over the years in premiums equal to the death benefit, but how long to you have live to actually equal that amount? Unfortunately if a person’s only option is to purchase a guaranteed issue policy, it’s because they have some serious illnesses that can or will eventually cause their death. Chances of dying sooner are much higher than passing in later years. You can’t lose and you won’t earn 10% interest on your money in a bank!