Medicare Supplement Plan F

COMPARE MEDICARE PLAN F COMPANIES AND RATES

Medicare Supplement Plan F is one of 11 different standardized Medigap plans. It is the richest Medicare Supplement level of coverage available for purchase. Each company that sells Medicare Supplements can sell any of the plan designs and do not have to offer all of them. If you weren’t eligible for Medicare prior to January 1, 2020 you cannot purchase an F plan, but who ever has it can keep it.

Just to clarify, Medicare Supplement and Medigap mean the same thing. The terms are used interchangeably, but they are NOT Medicare Advantage plans. Medigap and Supplement policies are secondary to Medicare. They pick up certain services that Medicare pays most of the costs, but not all.

All Medicare Supplements (Medigap) cover one common denominator, the Medicare Part B Basic Benefits. Basic benefits are the 20% of Part B services that Medicare does not cover. If you do not have any Medigap plan, then you will be responsible for an unlimited amount of out of pocket costs for the 20%.

Should you purchase a Medigap Plan F?

Plan F is not an option for you if you became eligible for Medicare after January 1, 2020. As long as you had either Medicare Part A and/or B prior to 1/01/2020 you can purchase a plan F for the first time or change to another F plan.

Just by looking at the chart, most people will initially look at the F plan because it has the highest level of benefits. What many people don’t consider is that sometimes they are wasting there money on “the best Medicare Supplement“. Everything is a trade off of paying the higher price and what you get in return.

For some people, paying a higher premium to not have to deal with minimal bills they get from a provider is worth the extra money. For others, saving $200 to $500 a year is worth looking at a medical bill and paying out a small amount. We recommend at least checking out plans G and N.

The ONLY difference between the Medicare Supplement plan F and G is an annual deductible. If you don’t mind writing a check for Medicare Part B Deductible for of out patient medical care, the savings can be significant.

If you are a little older and plan G is not giving you a large enough difference, then try looking at Medigap plan N. The N plan has 2 more additional differences. You MAY be billed up to $20 for an office visit and you will pay $50 for an emergency room visit if you are not admitted. If your physician accepts Medicare assignment, you would owe nothing. Remember you will also be responsible for the $183 Part B deductible.

For this instance we’ll use a 75 year old non-tobacco Male again in central Ohio. In this case plan F would cost $200.42 and the N plan is $138.94. That’s a savings of $737.76 in premiums for the year. I want to caution you that Plan N does not cover Excess Part B charges. If it is a possibility that you would receive medical care outside of the seven states that prohibit this expense, it won’t be covered and you should go with the G or F plans.

Keep in mind the older you are, the bigger the difference in price. Take into consideration not only what the plan costs today, but also that it will likely go up in cost with every year you get older. On the flip side, the older you are, the more likely you are to use more medical care and may not want to be bothered with the bookkeeping of paying a few bills.

What does Medicare Supplement Plan F Cover?

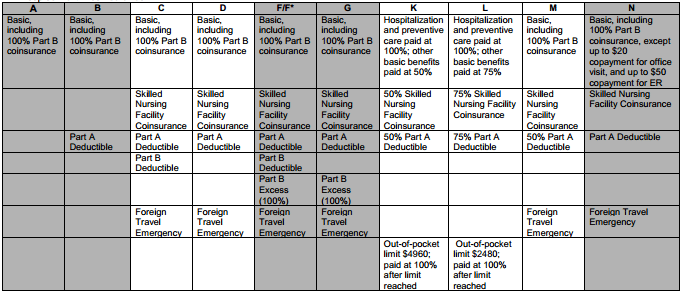

The chart below shows all of the Standardized Medigap plans available. Notice that some of the plans are highlighted. This is because the example used below is for a company that chooses to only offer the highlighted plans. Each company can choose the plans they want to offer. In this case, the company is offering plans A, B, F/HDF, G and N.

Medicare Supplement plan F covers all of the remaining 20% that Medicare does not cover. Plans K, L and M cover a portion of the 20% and limits the amount you can pay out. Plans A, B, C, D, G and M covers all of the Part B services after Medicare pays.

Medicare Supplement Plan F covers all of the Skilled Nursing Facility Coinsurance. Plans A and B do not cover it at all. Plans C, D, G M and N will cover it in full and plans K and L pay a portion. There is no Skilled Nursing Facility Coinsurance for the first 20 days, but days 21-100 have a copay for each day.

Medicare Supplement Plan F covers all of the Medicare Part A Hospital deductible. Plans C, D, G and N also pay 100% of the part A deductible while plans K, L and M cover a portion.

Medicare Supplement Plan F covers the Medicare Part B deductible . The amount can, and typically will change each year. Only plans C and F cover this expense.

Medicare Supplement Plan F covers Part B Excess Charges. Medicare allows providers to bill the patient an additional 15% more than the “Medicare Approved” amount. There are currently eight states that do not allow this charge. If you live in Ohio, Connecticut, Massachusetts, Rhode Island Vermont, Minnesota or New York, it is not permissible for a provider to bill you any excess charges. In this case the C plan is identical to the F plan UNLESS you are receiving benefits away from one of these states. It’s important if you travel for any extended period of time to another state that does not prohibit the excess charges.

Medicare Supplement Plan F covers Foreign Travel Emergencies. Medicare does not cover any medical care outside of the United States. You can purchase a Medicare Supplement that does help with the expense for emergencies. There is a separate $250 deductible for the emergency care, and the Supplement will then pay 80% of the charges up to $50,000 in a lifetime. You will be responsible for the $250 deductible and 20% of the charges.