Medicare Supplement vs Advantage Plans- Compare the Differences

Understanding the differences and costs of Medicare Supplement vs Advantage Plans is simple and easy

MEDICARE SUPPLEMENT vs MEDICARE ADVANTAGE PLANS

Medicare Part B costs don’t have a limit

Choose something! Medicare by itself has no out of pocket maximum limit. Everyone on Medicare should have some type of coverage in addition to Medicare Parts A and B to limit their total out of pocket expenses. If you still have employer or union coverage, you should consult with them before you make a change.

When a client asks “what’s better…a Medicare Supplement or Medicare Advantage plan, the answer may be a Medicare Supplement if it’s affordable. If you can pay the monthly premiums consider buying a Medicare Supplement over enrolling in an Advantage plan. Supplement premiums for a are around $100 per month for a 65 year old in most parts of the country. You won’t be limited to the doctors and hospitals you can use and you don’t need to get a pre-authorizations or referrals. There are more options available and easier access to care with a Medicare Supplement vs Advantage plans.

DIFFERENCES BETWEEN MEDICARE SUPPLEMENT vs ADVANTAGE PLANS

Medicare Supplements (Medigap)

Medicare Supplement plans pick up what Medicare doesn’t cover. The most common cost to you is the 20% of Part B Services and the Medicare Part A hospital deductible. You’ll continue to use traditional Medicare parts A and B. In general, Medicare covers the 80% of the bills and the supplement pays the difference based on your based on your plan benefits. Medicare Supplements do not cover prescriptions, so for full protection, you need to buy a Medicare part D drug plan too.

There are 12 Medicare Supplement plans. Medicare Supplements are classified by the following letters: A, B, C, D, F, HDF, G, HDG, K, L, M and N. Don’t confuse Medicare Parts A, B, C and D with Medicare Supplement plan names.

Medicare Supplement benefits are identical from company to company, but the premiums will be different. Supplement companies don’t control what doctors and hospitals you can choose from. You’re allowed to use any doctor, lab, skilled nursing or hospital in the United States that accepts Medicare. There’s no provider networks and you don’t need to get referrals or pre-authorizations from the insurance company for treatment.

Popular Medicare Supplement plans

Medicare Supplements cover different medical expenses depending on the plan. The majority of consumers choose a plan that pays all or most services at 100%. The most common Medicare Supplement plans are F, G and N. If Medicare covers a service, but not 100%, Plan F will pick up the entire difference. Plans G and N pay everything that Medicare doesn’t with the exception of a few small costs. If you choose the G plan, you’ll pay the Medicare Part B annual deductible. If you choose N, you’ll pay the Part B deductible plus $20 for an office visit, and $50 for an emergency room visit.

You Should Purchase a Medicare Part D Prescription Plan With Your Supplement

Add a Medicare Prescription Drug plan called “Medicare Part D.” Medicare contracts with private insurance companies to provide the prescription coverage. Companies have different premiums, copays and drugs that are covered. Medicare Drug plans are approximately $15 up to $100 per month, but there are medications that can cost even $1,000 per month without any coverage.

You will pay a 1% per month penalty if you don’t get Medicare drug coverage when you are first eligible.

Medicare Advantage Plans

Medicare Advantage plans cover all the services that traditional Medicare covers, but you have copays, deductibles and co-insurance for the services. If the person had traditional Medicare A and B with nothing else, they would pay the Part A Deductible for the hospital admission. Make sure you understand the guidelines for when you can and cannot make a change.

When you enroll in a Medicare Advantage plan, Medicare pre-pays the Medicare Advantage plan a fixed amount per month to provide your medical care. The amount that Medicare pays is based on the geographic area you live in. After Medicare pays the Advantage plan, they are out of the equation. Now it’s up to the Advantage plan to provide your medical care.

HMOs vs PPOs

HMO Advantage plans use a “gatekeeper” who is your primary care physician. For most HMO plans, the PCP helps to limit unnecessary specialist visits and tests. Some HMOs won’t require you to get referrals for specialists. If you join an HMO, you must use doctors and hospitals that are in the network. If you don’t, you will have to pay 100% of the bill. covered.

Some Advantage plans offer PPOs which allow you to go out of network. If you join a PPO instead of an HMO, you’ll pay a higher copays, deductibles or co-insurance, but you have the option of going out of network.

Eligibility

Both Medicare Supplements, sometimes referred to as Medigap Plans, and Medicare Advantage (MA) plans require you to have Medicare Parts A and B. You have to at least age 65, or be collecting Social Security Disability Income if you’re under 65.

- Part A (Hospital and Facility coverage) Medicare Part A services include charges during an inpatient stay in a hospital or skilled nursing facility. You earn Part A by paying Medicare taxes when you were working. It’s awarded automatically if you earned at least 40 credits toward Social Security. It won’t you cost anything additional if your age 65 or qualify for Social Security due to a disability.

- Part B (Medical coverage) Part B services include doctor’s office visits, outpatient therapy, surgery, tests or treatments. If you’re not going to collect your Social Security when you turn 65, you will need to enroll in Part B either online at Medicare.gov, over the phone or in person at your local Social Security office. The cost of Medicare Part B is determined by Medicare and typically goes up each year.

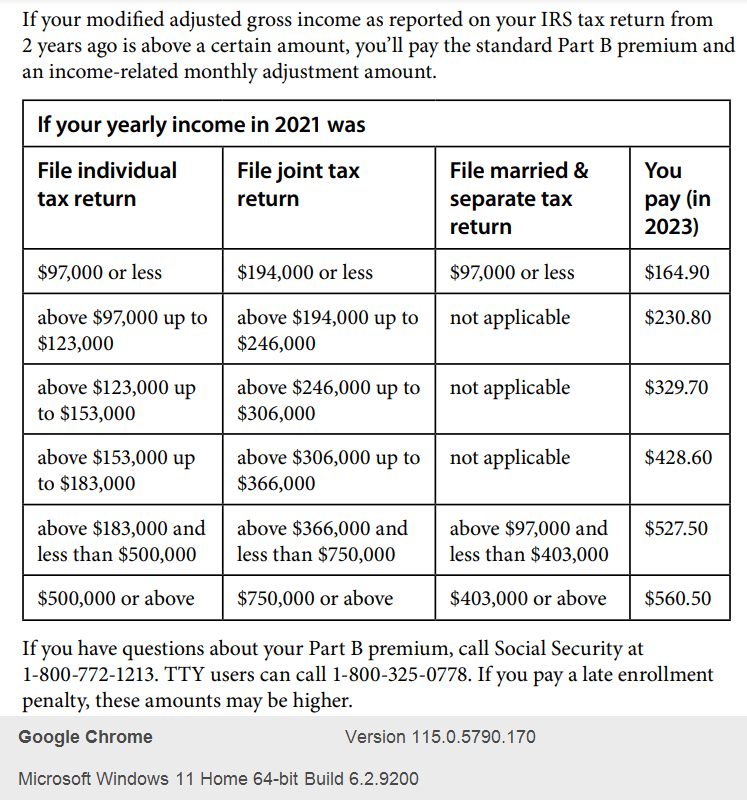

Determine How Much you’ll Pay for Medicare Part B

You’ll pay the basic Medicare Part B premium or a higher amount based on the your income. Most Medicare recipients pay the base premium, but if your income is more than $88,000 this year, you’ll pay more.