High Deductible Plan G Medicare Supplement

Fill out the form to get your Customized Quote for a High Deductible Plan G (HDG)

What is a Medicare Supplement High Deductible G Plan?

The High Deductible Plan G is a cost effective plan. The HDG covers all the benefits of a regular Plan G after you pay an annual deductible. The Deductible is set by Medicare every year, and usually increases each year by less than 2%. The HDG annual deductible for 2023 is $2,700.

You’ll make out by paying ultra low premiums. If you’re new to Medicare or recently retired, you can probably relate the idea to options you had before Medicare like HSA and FSA options. Those plans have lower premiums in exchange for some financial responsibility on your part. The idea is that you pay smaller expenses yourself, until you reach your deductible. This is the same concept but even better!

The biggest misconception about a High Deductible Medicare plan is that you have to pay all the costs before the plan kicks in. The reality is that Medicare Parts A and B pay all along the way. Even though you have an annual deductible, Medicare Part B starts paying 80% of the bill almost immediately.

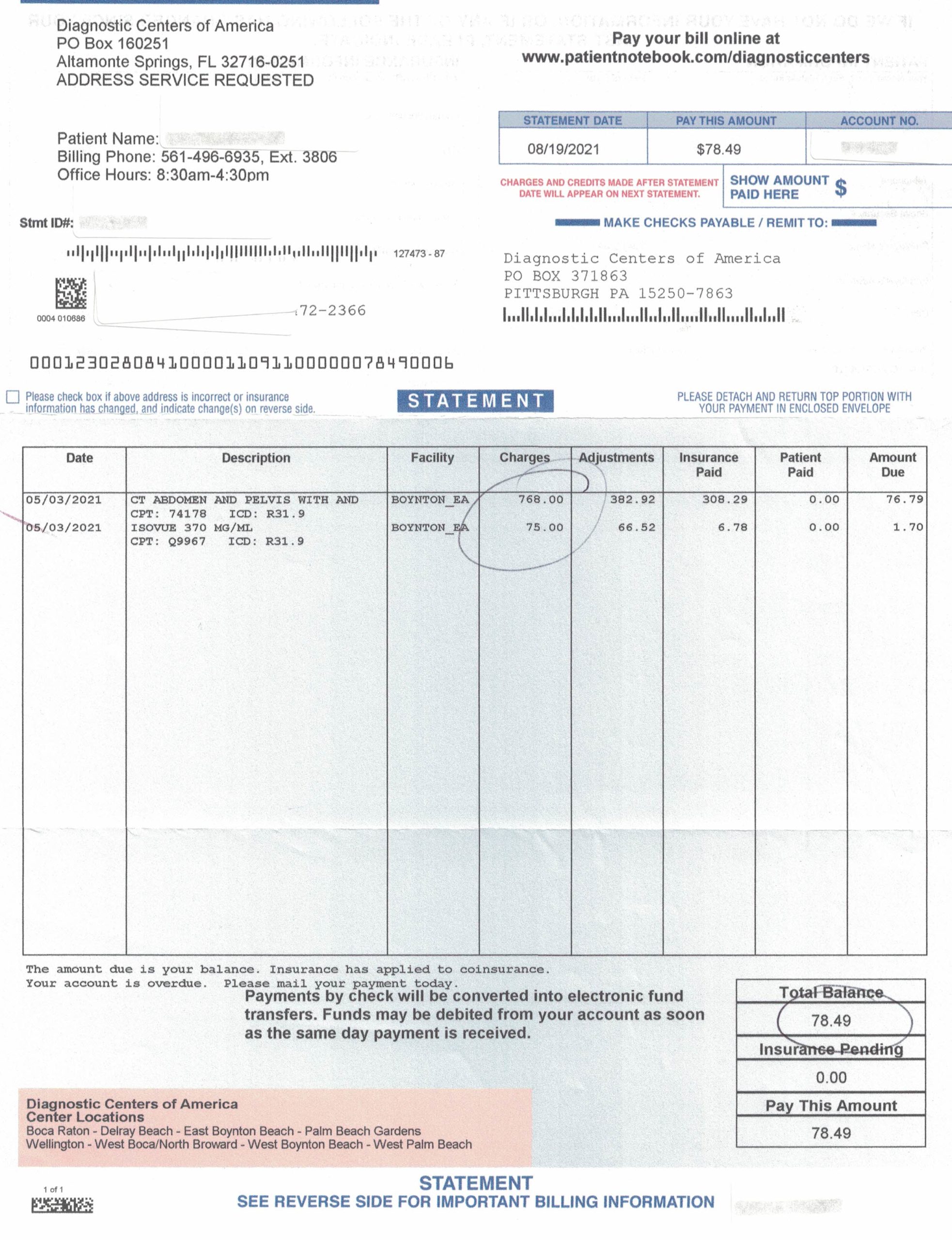

You’ll pay the first $226 for the Part B deductible which also goes toward meeting the annual HDG deductible, and then Medicare starts to pay their 80% portion for outpatient services. Here’s a copy of an actual bill for a CAT Scan from a HDG policyholder. You can see that the retail cost of the service was $843.00, but the patient responsibility was only $78.49

PLAN G BENEFITS

- Part B Coinsurance and Copays

- Part B Excess Charges

- Part A Coinsurance and Copays for Hospital Stays (Up To 365 days after Medicare benefits are used)

- Skilled Nursing Facility Copays

- First 3 Pints of Blood

- Part A Hospice

- Durable Medical Equipment (DME)

- Foreign Travel up to $50,000

How Does the High Deductible Plan G Work?

Here’s a simple example.

- Dr. billed $250

- Medicare Allowed $150

- Medicare Covered 80% of the $150.00= $120

- You are responsible for 20% of the $150.00= $30

- You pay the $30 which goes towards meeting the $2,700 annual deductible

Your deductible is now at $2,670. Now lets say you have an MRI.

- Outpatient Imaging billed $800

- Medicare allowed $400

- Medicare covered 80% of the $400.00= $320

- You are responsible for the 20% of the $400.00= $80

- You pay the $80 which goes towards meeting the $2,700 annual deductible

Your balance on the deductible $2,670 less $80 equals $2,590.

Now the doctor says you need to be admitted to the hospital. Medicare Part A has a $1,600 hospital deductible. It won’t matter if you stay 2 days or up to 60 days, the hospital portion of the bill will be $1,600.

- Hospital billed $10,000

- Medicare Allowed $6,000

- You are responsible for the Part A Deductible $1,600 (An amount set by Medicare each year)

- Medicare pays the balance of the Allowed amount

- You pay $1,600 which goes towards meeting the $2,700 annual deductible

The balance on your deductible is $2,590 less $1,600 leaves and you with $990.

How Much Does a High Deductible Plan Cost?

If you’re turning 65, the rates range anywhere from $30 to $90 per month for a females and $35 to $100 per month for males. Rates will differ depending on the company and where you live. You can see that if you only go to a doctor a few times a year and have an occasional diagnostic test, you’ll pay very little for your medical care, but save a lot on your premiums.

Is a High Deductible Plan Right for You?

This is a great option for people who haven’t experienced a lot of problems with their health. Some say “why should I pay so much if I never use it”, and if your that person, then an HDG plan may be a good option. If your looking for a plan that won’t increase very much over the years, this is definitely the way to go. Rate increases on High Deductible plans historically have been a lot lower than regular plans. In some cases, the rates even decreased over time.

It’s also a viable option if you’re older and your premiums are more than you would pay for the annual deductible plus and HDG premium.

It may not be a good option for a couple of reasons.

- You’ll need to keep track of your bills and pay the provider your portion until you hit the deductible. Medicare will send you a quarterly Explanation of Benefits to help you do this. It may be too much hassle than it’s worth especially when you have multiple charges from several providers.

- You could end up paying more out of pocket if your total medical expenses plus the HD premium are more than what your total premiums would be with a regular plan.

- Once you enroll in a HD plan, you may not medically qualify to go back to a regular Medicare Supplement.

What’s The Difference Between a Medicare Supplement High Deductible Plan G and High Deductible F (HDF)?

The bottom line is that there is no difference between the two plans. The only difference is the plan you’re eligible to apply for. If you were eligible for Medicare before January 1, 2020 you can still purchase an F or HDF. If you weren’t eligible for Medicare before then, need to enroll in a G or HDG plan. Some insurance companies offer both the HDF and the HDG in your area. There are a select few than charge the same premium for both plans too. There may be special rules that each insurance company has if you’re applying in a Guaranteed Issue enrollment period to designate which plan you have to enroll in.

Here’s the logic behind the bottom line difference – The Part B deductible of $233 under a HDG plan (2021) goes toward the total deductible of $2,490. That may sound hard to believe and difficult to understand, but the annual deductible equals the total out of pocket cost and it’s the same for both plans…$2,490.

COMPANIES THAT OFFER HIGH DEDUCTIBLE PLANS

Not all companies offer High Deductible Medicare Supplement Plans. In fact, most companies don’t. There are only a handful of companies that offer the HDG and High Deductible F (HDF) plans. United American, Medico and Humana offer both in most states. There are a few other companies that also offer High Deductible plans including Cigna, Bankers Fidelity and Omaha.